Even if you aren’t considering blockchain for payment, you shouldn’t dismiss blockchain technology altogether. When we first examined the future of blockchain and B2B, the focus was on cryptocurrency. But blockchain uses in B2B extend beyond Bitcoin and other cryptocurrencies. Blockchain technology has a future in smart contracts, supply chain security, and maintaining secure records.

Blockchain Technology for Dummies

For all cryptocurrency buzz, few people really understand how the underlying blockchain technology works. In it’s most simple form, blockchain technology is just a decentralized, distributed, digital ledger. It records transactions across computers in a peer-to-peer network. A record can’t be altered without altering all the blocks in the chain and changes require the consensus of the network. The mass collaboration is achieved by solving complex algorithms. Still confused? Take a look at this.

Because the block cannot be altered retroactively, blockchain technology is incredibly secure. And that security is what holds such promise for blockchain uses in B2B.

Trends in Blockchain for B2B Commerce

Of course, payment processing is the biggest trend in blockchain uses. But it isn’t limited to cryptocurrency. MasterCard, the global credit card company, recently filed a patent in the United States for blockchain technology for use in point of sale credit card transactions. To be clear, this isn’t cryptocurrency, but the application of blockchain technology to foil credit card skimming devices at the point of sale terminals. The cardholder, merchant, and MasterCard all reap the benefits of the additional security while thieves and their skimming devices are relegated to the dumpster. What is the implication for B2B? Well, anything that makes card processing more secure lowers costs for all companies (B2B or B2C) that accept cards. Reducing fraud benefits all business.

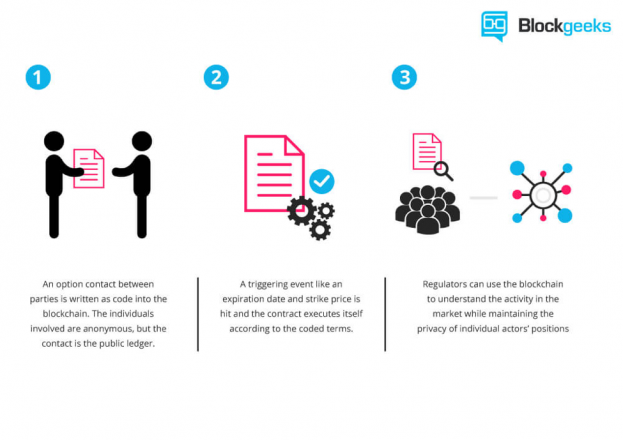

SmartContracts are another way that blockchain and B2B go hand-in-hand. They won’t replace lawyers, but SmartContracts will make issuing and enforcing contracts much easier. Here’s a visual representation of how SmartContracts work.

SmartContracts can be used to execute purchase orders, property rental agreements, and manage crowdfunding. It’s a way to exchange anything of value. SmartContracts are a secure way to simultaneously set out the conditions of an agreement while enforcing the terms too.

Supply chain management is another area where blockchain and B2B go hand in glove. Traditional supply chains are hampered by paperwork. Forms must pass through many hands for approval and every hand represents a fraud opportunity. Blockchain technology makes transactions more secure. This security is especially valued for doing business in emerging markets. Using an “if-then” scenario, manufacturers can agree to deliver goods on a COD basis with a carrier such as UPS. Delivery of the goods and collection of payment triggers actions by suppliers up the chain. Everyone is secure. Supply chain management is more effective too. With real-time data, management can make better decisions regarding purchasing, inventory, investments and financial positions.

The ability of this technology to secure data makes blockchain and B2B manufacturing perfect partners. Some manufacturers are required to maintain secure records. This ranges from the unique serial number assigned to medical implants and devices to the vehicle identification numbers on tractors, trucks, and cars. Once the part is manufactured and the unique identifying number is entered into a block it cannot be altered. Rolls of printed circuit boards can be tagged and certified as genuine. When liability issues arise, or the parts are subject to recall or similar government action, the manufacturer is assured their records are accurate and complete. In addition, buyers are assured their goods are not from the grey or black market. Counterfeit goods are much easier to identify. This same data security feature makes blockchain technology particularly appealing to maintaining healthcare records. It is almost impossible for an unauthorized user to access the data.

Barriers to Blockchain Uses in B2B

The largest barriers to blockchain use in B2B relate to cost and speed. Remember, every transaction requires executing code across the network. Each block must be encoded in a process called cryptographic hashing. Hashing requires computationally intensive code to arrive at the hash. The hash is nothing more than a fixed-length string of characters that begins with a specified number of zeros. In addition to all this hashing, the ledger must continually check itself for accuracy. This accuracy check requires code to run across the entire chain. These computations devour energy. Just running Bitcoin requires the same amount of energy consumed by a small city every day. Even if your blockchain is quite a bit smaller than Bitcoin, it still is an energy hog. Top tier technology research institutions like MIT and Cornell University are studying the energy consumption problem and developing solutions. This barrier should fall away soon.

But, even if every computer in the blockchain is processing at maximum energy efficiency and top speed, blockchain transactions are processed slower than transactions in a central database. So, faster processing speeds are not a given for simple transactions. The limit to the number of transactions per second is one reason that Amazon doesn’t accept cryptocurrency as a payment method. So, SmartContracts might not be best suited for simple transactions but saved for a complex global transaction with multiple players.

The Future for Blockchain for B2B Commerce

Blockchain technology and B2B commerce should have a long and profitable relationship. In a recent thought-piece on blockchain and B2B, Yoav Kutner, founder and CEO of Oro, Inc., noted that “blockchain can facilitate many things, from the transfer of financial securities to gift cards, mobile minutes, energy credit – even loyalty points” and identified blockchain technology as “one of the most important technologies to shape the infrastructure of the next generation of financial transactions”.

The potential of blockchain technology can’t be ignored. Leaders in B2B should invest in understanding the technology so they are positioned to evaluate possible applications. Like with any new technology, a risk and reward analysis is necessary before adoption. In the meantime, don’t dismiss the new opportunities presented for blockchain and B2B.