The new PSD2 regulations make open banking a reality for the E.U. But can this open the door for your company to realize more revenue efficiently? Will open banking open the door for new markets, new products, and new business? Open banking for ecommerce businesses can lead to faster and cheaper payments boosting the bottom line. For fintech companies, open banking provides almost unlimited opportunities for new products and new applications. For banks and financial service companies, open banking means a new way of looking at their business. Much like the internet of things, open banking in general and for eCommerce businesses opens the doors to products and services that were not even imaginable three years ago. With open banking for B2B commerce gaining traction and becoming more accessible, it might be an option to consider for increasing revenue and expanding your business.

What is Open Banking?

In open banking, a third-party that is not a bank can have access to account information via eCommerce APIs (application program interfaces) if the account holder provides consent. In the UK, access to these APIs must be free. In the E.U., open banking was ushered in under the revised Payment Service Directive (PSD2) and does not require APIs to be free. The idea that non-bank entities would have access to financial account information isn’t necessarily a new idea. Afterall, PayPal and Venmo are not banks, even though they facilitate the transfer of funds between businesses and individuals alike.

For years, electronic payments were made as banks issued credit cards and offered credit card processing services. They acted as a third party between buyer and seller. Under PSD2 in the E.U., sellers can opt to become Payment Initiation Service Providers (PISPs) and cut out the third party. With the use of APIs, payments have gone from electronic to digital.

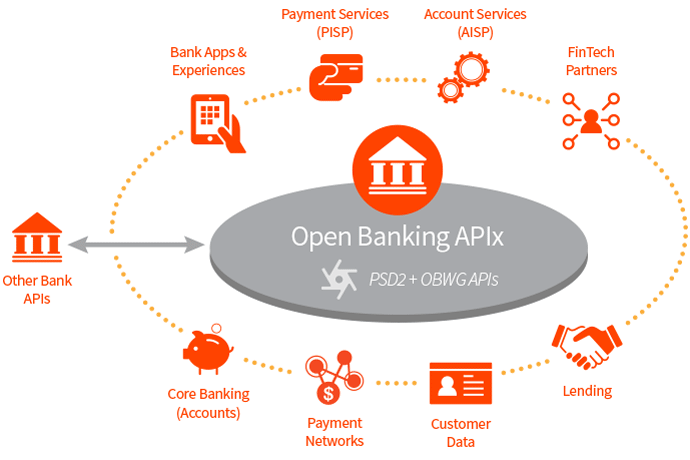

Open banking creates a network of accounts and data across institutions. Permission-based access to the network and data is available for consumers, financial institutions, and third-party service providers.

It looks a bit like this:

Think of it as a new trade route for the digital age and a way digital partnerships will be made in the future. With open banking, companies and developers can build new products and services by accessing and integrating their customer’s banking data (with permission) into their applications. Lending is easier and more secure and payment processing is streamlined.

While this might be unchartered territory, it isn’t the wild west. It is regulated, and rightly so. Because financial information is involved, security (think PCI DSS eCommerce compliance) is of the utmost concern. The regulating authority and the type of regulation varies from country to country and within economic trade areas. In most areas, it’s been a top-down approach to regulation.

For example, Australia’s open banking mandate only initially applied to the four largest banks but in the E.U. PSD2 is broad reaching. One exception is China, where their drive for a cashless society is more market driven. However, given that the government ultimately controls the markets, this bottom-up approach is ultimately being driven from the top-down. Needless to say, checking the regulations for the markets where you operate is a must before planning any open banking implementation.

How is This Being Implemented?

Open banking is made for eCommerce. And it isn’t just for B2C e-retailers either. Think about account to account transfers that don’t require the use of a credit card and you can see the appeal of open banking for B2B eCommerce in particular. After all, B2B buyers are looking for a wide variety of payment methods. So, it’s no wonder that it’s catching fire around the world. It’s like the traditional automated clearing house (ACH) where the clearing house is replaced by an API.

In Malaysia, InstaPay is a new product that combines the convenience of an eWallet with the freedom to shop brick-and-mortar locations with POS contactless purchases. Safely and securely.

In the U.K., since the implementation of open banking, 135 entities have been approved to provide open banking services leading to a plethora of fintech services.

The Berlin-based Open Bank Project has already built out over 250 APIs for over 40 banks and made possible new identity management. And with Trustly and Flywire, payers can initiate payments from a personal bank account in the currency of their choice. Paying for goods and services just keeps getting easier and easier. And eCommerce is all about reducing transactional friction.

Open banking APIs created a new frontier for fintech companies like Plaid. Their open banking for B2B commerce products are used by companies such as Betterment to create their own suite of B2C financial products.

Challenges to Open Banking

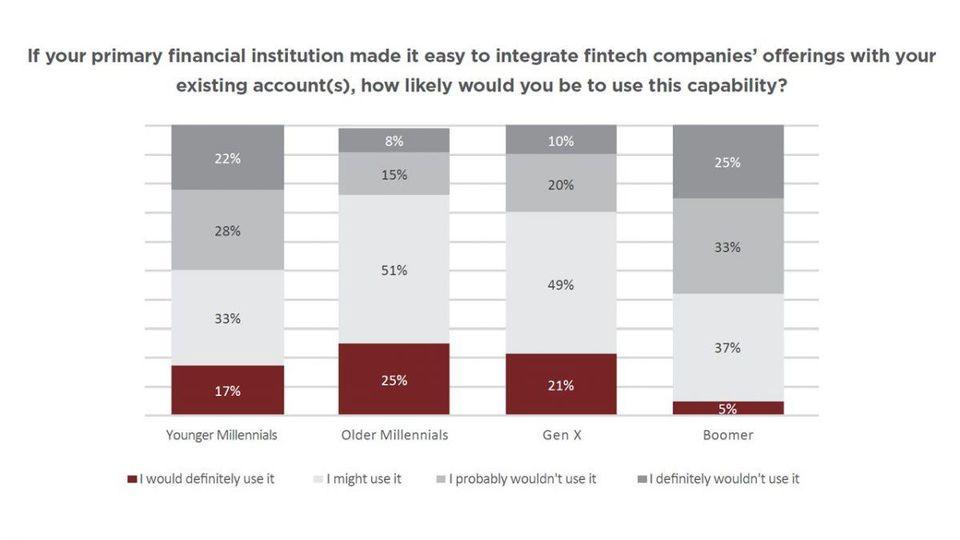

The greatest challenge to open banking is its less than universal open implementation. Much like Japan once walled off it’s country from the outside, the United States has not embraced the open banking movement, much less made any sort of move to implement it. In fact, unlike many Asian and European countries, in the U.S., there’s no law or regulation that requires a financial institution to make a consumer’s financial data available to third parties even when the consumer provides consent.

So, there’s that. But that doesn’t mean the market won’t pressure the government to act in the U.S. In a survey of U.S. consumers, Millennials and Gen X’ers showed great interest in integrated products made possible by open banking.

Another challenge is posed by smaller and local banks and credit unions that are having trouble joining the age of open banking. That’s because many do not own their tech stack. When you rely on others for your core services, innovation and compliance is hard. Now small institutions can partner with larger institutions to some degree and to some degree they are. But you will reach a point where these partnerships just don’t operate at scale. They will need a real platform and not just a partnership. And there are currently over 6,000 credit unions in the U.S. Even if open banking were implemented tomorrow in the U.S., that’s a huge number of institutions not ready for the tech challenge.

There’s also the sharing mentality. IT people love to throw around the “data is the new oil” adage. But honestly, who really shares oil? No one. Oil is a commodity, and nobody shares it freely. The free sharing of data under open banking seems contrary to market mentality. But that will change over time.

In addition, it’s easy to lose sight of the goal of open banking, which is more services, better and more secure services, and more transparency in transactions. Too often the focus becomes moving the data and forgetting why the data must be moved. The code may be ever so elegant and the app quite slick, but does it perform a service people actually want? In other words, developers and fintech companies get busy creating a hammer and nail when what consumers really want is to hang a picture. Its crucial that new product development be interdisciplinary. The new product team should include marketing, product development, and banking partners too.

As open banking gains traction, most of these challenges will be overcome.

Opportunities for Business

The obvious opportunities with open banking for B2B commerce is to speed payment, reduce the processing costs for payments, and make each transaction as smooth as possible. With data so accessible, accounts can be opened and approved at the speed of digital. In addition, sellers that opt to become a PISP can directly collect. No need to wait for a check to clear the ACH and no processing fees from a debit card, credit card, or wire transfer. It’s a rigorous process to become a PISP but if your business handles large transactions and is looking to reduce those large associated fees, this may be a real cost-cutting opportunity.

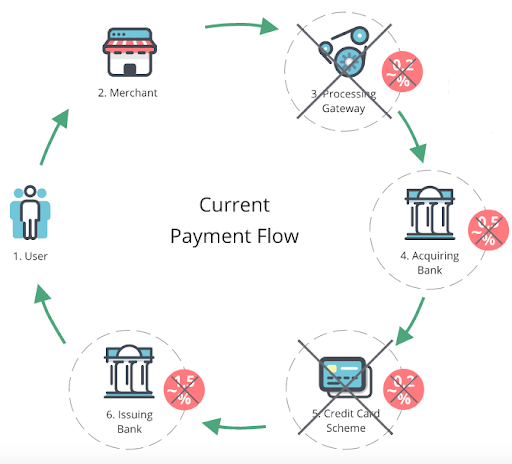

As you can see, with a simple API, the current payment flow that includes processing payment gateway fees and includes an issuing bank and an acquiring bank as well as the merchant and user can be cut down to simply the merchant and user. Replacing fees with an API and acting as your own PISP can be a real cost saving opportunity.

But the real opportunities lie with the banking and fintech companies. The field is ripe for the development of automated accounting apps, streamlined lending, and improved identity and financial security products. Open banking for B2B eCommerce means factoring and receivables lending should be easier than ever.

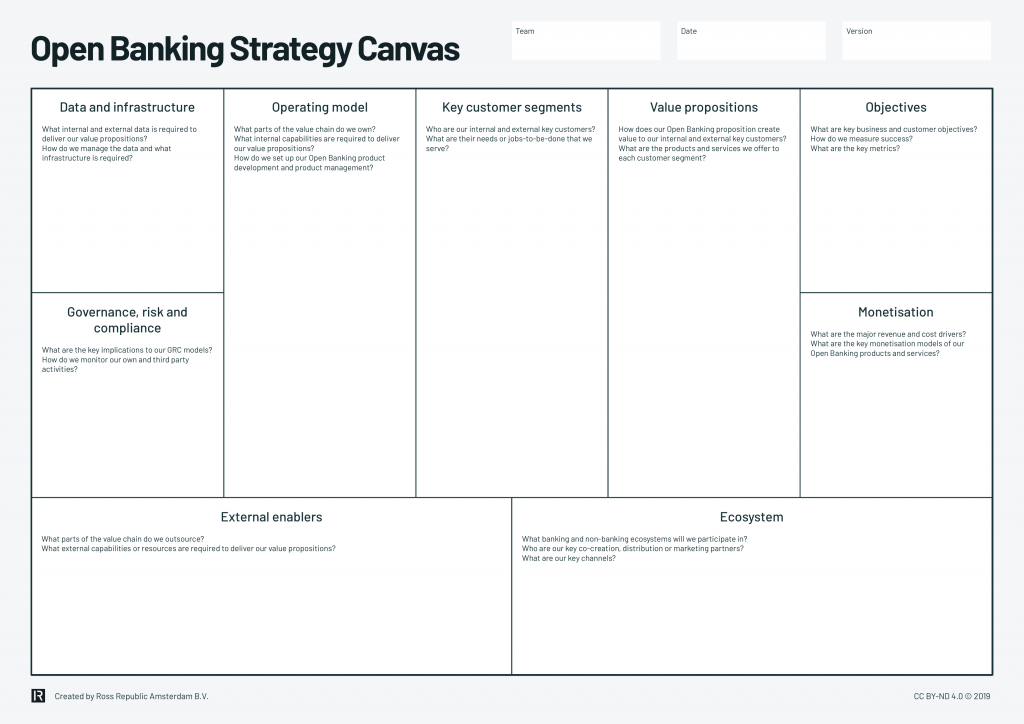

To avoid the trap of the slick app that has no marketability (as discussed in the challenges above) your new open banking products should build on your existing product strategy. Ross Republic has created a strategy canvas to help avoid this pitfall.

On this canvas, the customer is the focus of the blocks on the right-hand side and the back-end is the focus of the blocks on the left hand side. Notice that you start with customer and key business objectives and then bring them into alignment. Then you can freely ideate the products and services that can be built around the data.

Open Banking and the Future

What does open banking mean for the future? It depends on how the implementation shakes out. In one scenario, everyone complies, and no one innovates. This seems unlikely given the new products already reaching the market.

What’s more likely is that tech giants will arise and may even displace the role of banks in the economy. Imagine an economy where tech giants like Amazon or Alibaba leverage their size to get into the lending business. Apple might cut the need for a debit or credit card to be associated with ApplePay. Your paycheck might be directly deposited to a yet to be invented Google cash in the future. For banks, they will need to create their own digital strategy or be disrupted out of the marketplace. Hard to believe, but who thought printers would one day be able to order their own ink?

Of course, banks might fully embrace technology and become the tech giants. They may build their own payment networks and integrate directly with large retailers. Or retailers might embrace acting as their own PISPs and turn the tables on the banks.

One thing we know for sure is that the idea of open banking and the implementation of open banking will certainly impact how business is transacted. It’s an issue to continue to watch now and in the future.